Welcome to VIPsight Asia - Japan

|

|

| Nicholas Benes |

23 January 2022

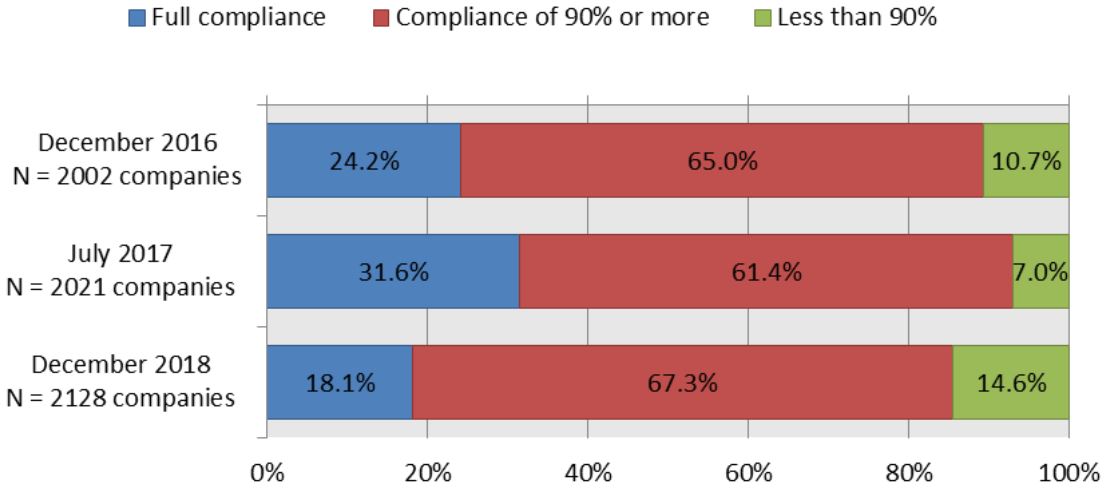

Results of "Availability of English Disclosure Information by Listed Companies" Survey for FY2021

- 88.9% English disclosure among companies selecting Prime -

Since 2019, Tokyo Stock Exchange, Inc. (TSE) has been conducting surveys on the availability of English disclosure information by listed companies and providing a list of the results through its website to a wide range of people including overseas investors. By doing this, TSE aims to understand the situation with regards to listed company English disclosure and promote it further, thereby enhancing convenience for overseas investors and allowing them to make appropriate investment decisions based on information disclosed by listed companies.

TSE has carried out the survey for FY2021 and has now published an updated list, as well as summary of the results. Looking toward the market restructuring in April this year, the proportion of English disclosure by companies which selected the Prime Market, the market for companies centering their business on constructive dialogue with global investors, reached 85.8% (79.7% as of the end of 2020). If we include companies that have announced a plan to start disclosing in English on transition to the Prime Market, the English disclosure figure stands at 88.9%, which shows how the market restructuring is becoming a catalyst for progress of English disclosure initiatives among listed companies.

The revised Corporate Governance Code, to be applied after the transition to the new market segments, stipulates that "In particular, companies listed on the Prime Market should disclose and provide necessary information in their disclosure documents in English." (Supplementary Principle 3.1.2, second paragraph.) Given this, we expect greater enhancement of English disclosure going forward.

Read more <click here>

Results of "Availability of English Disclosure Information by Listed Companies" Survey for FY2021 (PDF)

29 January 2020

Publication of "Availability of English Disclosure Information by Listed Companies"

Tokyo Stock Exchange, Inc. (TSE) will start publishing "Availability of English Disclosure Information by Listed Companies", a list containing information on English disclosure made by listed companies. This new initiative will go toward satisfying demand from foreign investors to understand the kind of English information disclosed by listed companies, including when and where they are disclosed.

Compiled by TSE based on voluntary responses from listed companies, the list will be updated regularly to allow investors access to the latest information. For further information please view: https://www.jpx.co.jp/english/corporate/news/news-releases/0060/20200124_01.html

29 June 2019

Nissan’s governance report is a warning for all boards

Comment: The special committee’s investigation into governance issues highlighted by the Carlos Ghosn affair reveals a corporate culture that allowed the “concentration of authority” in the CEO and a board that felt unable to ask the necessary questions.

Just 20 minutes. That’s the time Carlos Ghosn allegedly allowed for each board meeting when he was heading Nissan.

Whatever the facts surrounding Ghosn’s guilt or innocence of the charges he now faces, that nugget of information stands out as a red warning light.

The disclosure that Nissan’s boardroom get-togethers were so brief comes in the report published this week from the car maker’s Special Committee for Improving Governance.

Headline writers were quick to highlight the report’s conclusion that a “personality cult” existed around Ghosn that made his behaviour “impenetrable territory” that could not be questioned.

The report says Ghosn “realised concentration of authority in himself” through domination of appointments and remuneration of senior managers. It alleges he cemented this power through the appointment of a single director, Greg Kelly, to run administrative affairs. According to the report, any questioning of remuneration or appointments, Kelly, or the so-called “office of the chief executive” were met with vague answers that gave little away.

At Nissan, the report says “dissenting views” could be met with suggestion that “they would be removed”.

What emerges, therefore, in the under-reported recommendations of the committee, is a strategic effort to drastically reduce the powers of the CEO at Nissan.

Those used to Western norms will be surprised to hear that the major prescription for improved governance will be to move Nissan from its current complex, “traditional” Japanese governance structure to a slimline “three statutory committees” system. In other words: audit, nominations and remuneration committees.

This is worth reflecting on. For many in business the process of distributing accountability through committees may be considered bureaucratic and mundane. But try functioning without it and the risks, as far as Nissan’s special committee is concerned, are all too clear.

Some of the other recommendations of the committee include:

- The majority of directors should be independent and from outside the company;

- The number of directors should be enough to prompt “lively discussion”;

- Diversity among directors should be “fully considered”;

- The nominations committee should have a majority of external, independent directors;

- One role of the nominations committee should be to refresh membership of the board “on a regular basis”;

- All members the remuneration committee should be external, independent directors;

- The chair of the board should be an independent, external appointment;

- Independent members of the board should meet regularly;

- Third-party providers should evaluate the effectiveness of the board, but the audit committee should also conduct audits in “respect to the effectiveness of the supervisory function” of the board of directors;

- Internal audit should report directly to the audit committee if it encounters “misconduct”. Directions to internal audit from the audit committee trump those from the chief executive.

The report highlights the need for corporate culture to change, not least switching attention from short-term aims to mid and long-term objectives. The CEO’s office will become subordinate to other departments and the rather opaque “CEO’s reserve” fund is to be abolished.

Rebuilding trust

Over-reliance on a single chief executive is always risky. However, it’s not hard to see how it happens if they appear particularly successful.

But there’s a further issue connected to Nissan’s report. The business world has for some time battled with a “trust” deficit. Ever since the financial crisis, a succession of corporate scandals and endless headlines shining a light on excessive executive pay, the discussion among business organisations and politicians has been focused on how to rebuild trust in business—indeed, how to rebuild trust in the capitalist system.

Reports of a chief executive who was “deified”, who could not be questioned, who built opaque corporate structures to duck accountability, only feeds into the public perception of business being much less than honest. It confirms the narrative of business suffering from moral bankruptcy.

What Nissan’s report recognises is that even high-flying CEOs are accountable to their companies, not the other way round. That’s something worth remembering, not just in Japan, but here in Europe too, where chief executive pay settlements seem to indicate that chief executives are treated reverentially.

The special committee concludes:

“Although it is a matter of course that business strategies shall be proposed on the CEOs’ responsibility, such strategies must be discussed by not only the board of directors but also management meetings such as the executive committee, and eventually, approved at the board of directors.

“SCIG [the special committee] believes that it is unfortunate for Nissan that under the Ghosn system, there is a perspective that no goals that it should reach had necessarily been discussed in an effective way in meetings of the board of directors or the executive committee and other management meetings.”

The board is there for a reason. It must be allowed to do its work, not least to actively prevent the “deification” of its CEO, to question and to challenge. Most of all, it should define an organisation’s purpose. Without those elements we will always see CEOs who come to believe their own propaganda.

NISSAN MOTOR CO., LTD.Special Committee for Improving Governance Report

Report

CHAPTER 1 PURPOSE OF SCIG’s FORMATION

PART 1 PURPOSE

NISSAN MOTOR CO., LTD. (“Nissan”) has resolved to form a “Special Committee for Improving Governance”atitsBoard of Directors Meeting on December 17, 2018. The Special Committee for Improving Governance (“SCIG”) was formed for the following purposes: to ascertain the root causes behind Nissan’s governance issues which led to the misstatements in Nissan’s Annual Securities Reports, etc.; to provide recommendations for the improvement of Nissan’s governance commencing with Nissan’s approval process for determining director compensation, and to provide recommendations for Nissan to create a healthy state of governance as a foundation for sustainable business asa world-leading company (the recommendations in and , the “Recommendations”). The purposes of SCIG do not include assigningany criminal or other legal responsibility to any individual or corporation.

<click here> complete version (PDF)

https://www.nissan-global.com/PDF/190327-01_179.pdf

29 June 2019

Tokyo Stock Exchange, Inc. published the "TSE-Listed Companies White Paper on Corporate Governance 2019" (English Version). TSE publishes the White Paper every other year by gathering data in the Corporate Governance Reports submitted by all TSE-listed domestic companies.

The 2019 analysis considers recent progress in corporate governance reform related to Japanese companies, including the revision of the the Japan's Corporate Governance Code.

TSE-Listed CompaniesWhite Paper on Corporate Governance 2019

Introduction

From the perspective of ensuring shareholder protection on par with international standards so that both domestic and foreign investors can participate in the market with confidence as well as enhancing corporate governance based thereon by illustrating corporate governance initiatives of all Tokyo Stock Exchange (hereinafter, “TSE”) listed companies and progress therein, TSE has made a comprehensive analysis of the current state of their corporate governance based on data in reports on corporate governance disclosed by listed companies (hereinafter, the “ CG Report ” ), and published the White Paper on Corporate Governance in every other year since 2007. This White Paper on Corporate Governance 2019 (hereinafter “ this White Paper ” ) is the seventh publication in the series.

Up until now, TSE has taken various initiatives, such as urging listed companies to enhance corporate governance in 1999, formulating the Principles of Corporate Governance for Listed Companies in 2004, institutionalizing CG Reports in2006, and introducing the independent directors/kansayakusystem in 2009. In 2015, the Japan’s Corporate Governance Code (hereinafter “ the Code ” ), which established fundamental principles for effective corporate governance at listed companies was formulated, and in June 2018, the Code was revised to further pursue corporate governance reform so that it is more substantial through engagement between companies and investors.

In the White Paper, analysis is conducted in consideration of recent progress in corporate governance reform related to Japanese companies. We hope that this White Paper will provide the stakeholders involved in these efforts with an overview of the state of corporate governance efforts by listed companies in Japan that undergo dramatic changes.

Finally, we would like to acknowledge the great assistance rendered by Daiwa Institute of Research Ltd. for the preparation of this White Paper.

May 2019 Tokyo

Stock Exchange ,Inc.

<click here> complete version (PDF)

https://www.jpx.co.jp/english/news/1020/b5b4pj000002xyda-att/b5b4pj000002xyfw.pdf

3 September 2012

“Shareholder Spring” - Even in Japan!

2012 seems destined to go down in history as the year when “shareholder spring” not only took root in Europe and the U.S., but Japan as well. In the wake of risk oversight errors by TEPCO, a massive 10-year fraud by Olympus, and a series of scandals in Japan and around the world, in June of 2012 a significant number of Japanese individual shareholders joined foreign and domestic institutions in voicing their distrust of corporate governance at annual general meetings.

It was as if a dike broke. Suddenly, more individuals were taking action by submitting shareholder proposals, voting against proposals submitted by management, or voting in favor of proposals submitted by other shareholders.

A change in the wind could be felt not only at the shareholder meetings of the electric power companies beset by the “no nukes” movement, and not only at lesser-known companies mired in family politics. Some household name-companies like Nomura Holding and Mizuho Financial Group received numerous shareholder proposals, - fully 17 by Nomura, and 10 by Mizuho. Not all the proposals were “wacko” or about environmental issues unconnected to economics. A good number related to legitimate shareholder concerns about corporate sustainability, oversight, managerial incentives, and governance.

If it continues, over the next few years this trend could have a significant impact on governance practices, the competitiveness of Japanese firms, and the fortunes of the Japanese stock market, which is now mired down with a price-book ratio (PBR) of .8%, Since this PBR is roughly one-half that of the average for developed nations, Japan’s stock market has a lot of potential upside. Recent events also show that domestic proxy fights – which are essentially hostile acquisitions of control - may be increasing in frequency (albeit from a small base). And according to a Russell-Nomura poll of 304 companies, this year the average voting support rate for shareholder proposals increased to 11.5%, up from last year’s 9.1%.

Happily for stock market prospects, there are several reasons why Japan’s “shareholder spring” is likely to accelerate over the next few years.

First, as a general matter, Japan’s Company Law gives shareholders very strong rights. To be eligible to submit a shareholder proposal, one only needs to hold the lesser of 1% of the company’s issued shares or 300 “units” of stock. Especially at current stock prices, in most cases 300 units is a number well south of US$10,000. Furthermore, unlike the U.S., which allows management to exclude proposals to nominate or terminate directors from the proxy materials, Japan has very few rules clearly allowing the exclusion of shareholder proposals from proxy materials.

The result is a more powerful legal infrastructure to promote “shareholder democracy” than exists in most other countries. After decades of almost total neglect, this infrastructure is now coming to be used by individual shareholders on a more regular basis. (At its most basic level, this is reflected by the fact that more people attended AGMs this year than last year, as suggested by the July survey by the Japan Investor Relations Association (JIRA).)

A second factor is that individual shareholders have been growing in numbers for more than 10 years, and now comprise about 30% of all listed company shareholders, a figure that is even larger than the approximately 26% held by foreign shareholders. Proactive individual holders in Japan are now waking up to the fact that if they vote similarly to foreign institutional holders on governance and sustainability issues, together they will comprise a formidable force. And the advent of internet voting at more companies makes voting easier. According to surveys by Nomura, about 40%-50% of individual shareholders now vote their shares, and only about one-quarter of them respond that they “vote with management on every single proposal”.

Clearly, the days are gone when most Japanese companies could sit back and depend on individual holders and financial institutions to support them. Simply from looking at their own shareholder base, companies are well aware of this. Daiwa Institute of Research calculates that “stable shareholder” Japanese banks and insurance companies now hold only about 7% of TSE-listed shares, down from 39% in 1986.

Third, the trend of “more shareholder proposals” has actually been gathering steam for the past ten years. As of 1992 shareholder groups, or individuals only submitted proposals to about five or ten companies per year, most of them related to nuclear energy. Most of them were related to the anti-nuclear movement. But in 2010, more than 40 different firms received shareholder proposals, about a much broader range of topics.

Last but not least, the very low share prices of Japanese companies, which have not recovered as much as prices many other stock markets, is itself a factor. In any country, no one likes to sell stock he bought for 4,000 Yen for 400 Yen, especially if that current stock price is trading well below net book value per share (as is the case for 67% of TOPIX companies). When stock prices are this low, shareholders who rationally think the company must have much higher intrinsic value and can afford to be patient (e.g., retirees who bought many years ago), tend to voice their complaints rather then sell.

What Made This Year Different

A confluence of scandals and value-destroying events during the past 18 months raised Japan’s fledgling investor renaissance to a “next level” of shareholder involvement and activism. In a nutshell, here is what was different in 2012:

1. Fukushima made people angry. In the Fukushima crisis, Japan had its own glaring, scary example of the huge destructive potential that arises when a company’s governance and risk management oversight does not independently consider issues that impact “sustainability” enough, and assumes that anything it can get approved by the regulators is acceptable. Said another way, the Japanese public had its own domestic case of massive “risk externalization” to ponder over, similar to BP in the Gulf of Mexico or the bankruptcies of Lehman and AIG.

2. The very topic of “Corporate governance” events was constantly in the news. Whether it was Olympus, Daio, Kyushu Electric’s political tampering, the third amendment of the Company Law in 10 years (still ongoing), or movements abroad such as “Occupy Wall Street” and “say on pay”, - the public was constantly reminded that there seems to be something wrong with the state of corporate governance. And with Japan’s price-book ratio (.9) at a level that is half the average for developed nations, many investors did not need much of a reminder.

3. For the first time, not all of the people putting forth shareholder proposals were unknown individuals who could be dismissed as “fringe elements”. Led by the popular Governor Hashimoto, the city of Osaka (as an 8.9% stockholder) submitted proposals to Kansai Electric, and made critical statements at the latter’s AGM, and Vice-Governor Naoki Inose of the Tokyo Metropolitan government led the charge for the Tokyo metropolitan government (a 2.7% holder) to submit four proposals to TEPCO’s shareholder meeting. These gentlemen repeatedly appeared on television to explain their opinions. For the first time in memory, making shareholder proposals was treated by the media as a legitimate procedure worthy of coverage, - whereas when anti-nuclear groups made proposals in earlier years, they were completely ignored.

Because of a new FSA rule requiring disclosure of per-item vote counts, this higher level of voting support was immediately disclosed and therefore publicly visible. Japan’s shareholder spring will now tend to accelerate because proposing shareholders have received clear feedback, for the first time, that reasonable proposals can attract enough voting support that they might actually have an impact on the stance that managers take in response, for example by provoking a change from “flat no” to “let’s compromise where we can”. (The best example of this prospect is the case of Mizuho Financial Group, described later in this article.)

This new rule was implemented by the FSA as of the June 2010 AGM season, as a result of requests for greater transparency about voting results by both foreign and domestic investors going back a number of years. It has generated a sea change in the market. Its full impact will take a few more years to sink in, but because of it we already know (for instance) that the highest approval percentage for a shareholder proposal was 38% this year and 48.5% last year. It seems quite possible that in the next few years, a shareholder proposal opposed by management may be approved…which will show that “it can happen”.

Not surprisingly, nearly half (48%, up from 42% a year ago) of those firms responding to the JIRA survey said they intend to look carefully at the shareholder proposals that got significant support, and analyze the reasons why.

4. Most importantly, a number of proposals were of the “generally reasonable” type rather than the “personal grudge” or “political” type, and often it was these proposals that received more support from other shareholders. They suggested changes that many investors could agree with in terms of corporate sustainability, improved governance, or enhanced investment efficiency, rather than unrealistic things like the immediate stoppage of all nuclear power generation. The result was higher levels of voting support for the “eminently reasonable” proposals.

Overview of Shareholder Proposals

There are generally three situations in which shareholder proposals have put forth in recent years:

1. Cases where control of the company is in dispute, and there is a effectively proxy fight under way. This year, this group included companies such as Accordia Golf (vs. PGM and an investor group); Aeon (vs. Parco); Eikoh Holdings (vs. Shingaku-kai); Yakult (vs. Danone, a 20% owner); and Yamada Corporation (internal). Sometimes, some sort of scandalous behavior or misuse of corporate funds is alleged as the pretext for the dispute, but the reality is that it is really control of the company that is at stake, not just improving governance practices or remediating the alleged offense. In such cases, unsurprisingly, the most frequent proposals made are those to appoint a different slate of directors and statutory auditors, and perhaps also to terminate certain members of the board.

Proposals were also submitted to a range of other firms including Toshiba, Japan Tobacco, Charle, Hoya, and family-controlled Suntec, to name a few examples.

Like Mizuho Financial and Suntec, Toshiba received a proposal to change its Articles to alter the present “pro-management” way that proxy cards are counted when they contain blanks, - that is, always in favor of management’s proposals, but against any shareholder proposals. This obtained 21% voting support, which is generally considered to be some degree of “success” for an activist shareholder.

Suntec received seven detailed proposals from the same investor (Mr. Nakayama) who made proposals at Mizuho Financial Group. Many of these focused on the governance practices and eliminating the company’s nepotistic board composition and management structure. Proposals to use capital surplus redeem treasury stock, and appoint an independent outside director, received respectively 22% and 23% support from shareholders. Other proposals, such as to require disclosure of director training policy, terminate the family board members, reform proxy card counting practice, generally received a bit less than 20% support, still respectable showings.

Japan Tobacco’s shareholders voted on several proposals from The Children’s Fund (TCI) related to increasing the dividend or buying back or cancelling treasury stock. These were defeated, but received support at the 16-17% support level. Charle’s shareholders wanted cooperation with a shareholder lawsuit, changes to the Articles restricting activities to core businesses, and disclosure of each director’s compensation. The proposals to were rejected, but received support at the 9-10% level.

2. Cases in which shareholders are seeking improvements in corporate governance structure and practice. In 2012, this included many serious and rational proposals, such as many of those sent by individual investors to Mizuho Financial Group. There, seven garnered more than 23% support and demonstrated the power of the “eminently reasonable” proposal. (See below.)

3. Cases where specific management policy issues are a principal driving force. This year, this group comprised most of the major electric power companies (including TEPCO, Kansai Electric, Tohoku Electric, Shikoku Electric, and Kyushu Electric); and Nomura Holdings.

At the power companies, while there were a number (both realistic and unrealistic) proposals to exit from the nuclear power generation business, or spin off the power distribution business, there were also a number of proposals more suitable for consideration at an AGM. Most notable among them were Tokyo Metropolitan Government’s (Vice-Governor Inose’s) proposals: a) to add language to the Articles clarifying that the mission of the company is the stable provision of electricity, focusing on good customer service (21% approval); b) to require TEPCO to disclose enough details of its cost-plus-based electricity pricing calculations to allow third-party confirmation of their appropriateness (arguably, a compliance or “sustainability” issue; 16% approval); or c) to further reduce costs and consider use of standard “smart-meters” to prepare for the competition-based electricity industry that will no doubt soon arise in Japan (14% approval).

Kansai Electric topped TEPCO’s 14 proposals, with 30 in total. In this group some of the more reasonable ones proposed: a) reducing the size if the board from 19 to 12; b) creating a CSR policy founded in the Articles; c) requiring the disclosure of compensation to individual directors (32.6% approval), as well as their ties to foundations or quasi-governmental bodies; d) requiring disclosure of information about electricity price increases; or more disclosure in general (30.8% approval); e) requiring deployment of smart meters and energy-saving policies (26.3%); f) permitting indemnification of outside directors, so as to facilitate their appointment (38% approval); g) appointing a certain independent director (the former CEO of Google Japan; 25.9% approval), or g) firing the current President. In total, eight out of the 27 shareholder proposals received more than 20% voting support.

At Nomura, there were 17 shareholder proposals, many of which can only be categorized as “troublemaking” (iyagarase) or even “absurd” – e.g. , change the short name of the company, abolish the “three banzai” cheer, change all company toilets to Japanese-style toilets, restrict executive compensation to minimum wage in case of low profits. To its credit, Nomura included them all in the proxy materials, even though it probably had legal grounds to exclude a number of them. In the author’s opinion such proposals do damage to the entire market by potentially tainting the image of all “activist” investors, including those who are constructive and conciliatory of mind.

Most meaningful was the fact that the current Chairman of the company, Nobuyuki Koga, only received approval from 70.3% of shareholders, and one of the independent director candidates, Tsuguoki Fujinuma (a Governor of the Tokyo Stock Exchange and outside board member at several major companies), only received approval from 65.9% of shareholders. In the world of shareholder meetings, these are very low approval ratios. A large number of “normal” shareholders were effectively saying, “don’t come back” or “we do not trust that you are sufficiently ‘independent’”.

Overall, Nomura’s proposals reflected the high degree of distrust with which certain members of the public – including its own unhappy shareholders! - view the company, a suspicion that the recent insider trading scandal may have simply confirmed. Together with Hoya, which last year was beset with a long list of detailed proposals, Nomura’s case serves as a reminder to companies that corporate image and the way they engage with their disgruntled shareholders can directly affect the quality of their AGMs as a constructive forum for beneficial communication, and vice versa.

But there were also a few arguably reasonable proposals, such as abolishing director indemnification (but not D&O insurance), requiring new share offerings take place via rights offerings, or abolishing upside-only stock acquisition rights. The first two of these proposals garnered 8.0% and 8.9 support, despite their flippant tone.

The Power of “Reasonable Proposals”: Mizuho Financial Group

As noted, this year not all of the people putting forth shareholder proposals were unknown individuals who could be dismissed as “fringe elements”. But more importantly, a number of proposals were of the “generally reasonable” type rather than the “personal grudge” type. It was these proposals that received relatively more support from other shareholders. They suggested changes that many investors could agree with in terms of corporate sustainability, improved governance, or enhanced investment efficiency.

The best example of the potential for a positive and constructive feedback loop arising from “eminently reasonable” shareholder proposals in Japan was set by Mizuho Financial Group’s AGM. Out of ten shareholder proposals were submitted by various individuals, eight were supported by more than 10% of all voting shareholders, and an impressive even received 23% or more voting support. Fully seven were supported buy ISS, the proxy voting advisor which influences the voting of many foreign institutional investors.

Not surprisingly, the proposal that received the most support was the most clearly “reasonable” one. This was a proposal that would have required Mizuho to simply disclose whether it had a policy for training directors about governance and the law, and if so, to disclose what that policy entailed, and the actual training undertaken during the prior year. Given that shareholders are asked to approve director candidates based on their qualifications and most Japanese believe that education and training are good things, it is not surprising that this proposal (#7) garnered the highest level of support of all, an impressive 28%.

Why are these numbers significant? First of all, they reflect a level of distrust about large corporations and their governance practices which has not been seen before.

Secondly, in most countries, even if it is not approved at the AGM, if a shareholder proposal is supported by more than about 20% of voting shareholders, it is considered a sharp rebuke of current management, which then is put under intense pressure to take some sort of concrete action on that item over the next year. Only by doing so can management hope to prevent the same proposal from being submitted again, whereupon it is almost certain to obtain more support simply because shareholders are irritated that, say, an opinion held by 25% of voting shareholders was completely and totally ignored. (Note also that since not all shareholders vote, it could easily be the case that a larger number of investors than 25% actually agree with the proposal, and may vote in favor of it next year.)

Below, I have set forth the substance of seven shareholder proposals made to Mizuho Financial Group by Mr. Yasushi Nakayama (a private investor and active trader who once worked at a bank) and others, all of which received voting support in excess of 23%. All of these were proposals to amend the Articles of Incorporation in ways that are hard to dismiss as silly or “fringe”. The translated sentences are those given by Mizuho Financial Group, except where word usage was incorrect:

“Proposal #6: (27% support) The Company shall instruct its subsidiaries that the Company administers, such as bank subsidiaries and securities companies subsidiaries, in exercising voting rights of shares held for strategic reasons, to exercise their voting rights appropriately by means such as seeking opinions from independent proxy advisers. [intended to prevent “blindly” supporting cross-held companies’ managers]

Proposal #7: (28% support) The policy, contents and results of the training provided by the Company and its consolidated subsidiaries for their board members shall be disclosed on the Company’s website.

Proposal #8: (27% support) The amount of compensation and/or bonus to be paid to Directors and Corporate Auditors during each fiscal year shall be described and disclosed — on an individual basis for such Directors and Corporate Auditors,…

Proposal #10: (26% support) The restriction on the number of characters in a description of reasons for a shareholder’s proposal shall be relaxed from 400 to 4,000.

Proposal #11: (28% support) With respect to voting forms for general meetings of shareholders of the Company, blank voting forms without indications of shareholders’ approval or disapproval should not be treated differently for the Company’s proposals and the shareholders’ proposals. [intended to prevent Mizuho FG from effectively voting blank proxy cards in favor of its own proposals but against shareholder proposals]

Proposal #12: (24% support) In principle, a Director is prohibited from acting concurrently as chairman of the meeting of the board of directors and CEO, and any of Outside Directors shall act as chairman of a meeting of the board of directors….[intended to split the roles of Chairman and CEO, with the former served by an outside director]

Proposal #13: (23% support) A liaison for whistle-blowing within and from outside the Company with respect to misconduct of in-house members of the Board of Directors shall be established at the Board of Corporate Auditors…..”

The Proposal Requiring Disclosure About Director Training (#7)

This proposal is not only fascinating to me on a personal basis, but also exemplifies why I believe we will see more “reasonable” proposals like it. In short, Mr. Nakayama made a cogent argument, and Mizuho responded in what other shareholders could easily see as an evasive, even lackadaisical response. From the proxy materials:

“Reasons for Proposal

The brief personal records of candidates for Directors and Corporate Auditors presently described in convocation notices for general meetings of shareholders are not sufficient to determine whether or not each candidate is an appropriate person for Director or Corporate Auditor when voting for such Directors and Corporate Auditors. Monitoring and supervising the Company as a whole is different from executing business in each department, and for the performance of board members’ duties, it is necessary for that person to be well-acquainted with his or her obligations as a board member as well as the general business, including areas he or she has not yet experienced. The level of such knowledge and the attitude held by not only candidates for outside board member positions, but also candidates from inside the Company who constitute the majority of the candidates, is not clear. Therefore, disclosure about board member training on the Company’s website as to its policy (the persons to receive training, the time when training is to be given and the type of training), contents (training details, training period and training provider) and results (persons who received and did not receive the training) can enable shareholders to approve candidates with confidence.

In addition, the Company’s responsibility is limited only to the duty of disclosure, thereby putting fewer burdens on the Company.

Opinion of the Board of Directors of the Company

The Board of Directors of the Company opposes this proposal.

The Board of Directors also recognizes that Directors and Corporate Auditors of the Company are required to have broad knowledge and attitudes as board members in order to perform their duties, and believes that such broad knowledge and attitudes as board members should be gained through experiencing various kinds of duties, etc.

When selecting candidates for Directors and Corporate Auditors, the Board of Directors determines as the candidates, persons whom it concludes to be appropriate as Directors and Corporate Auditors of the Company, based upon due consideration of the knowledge and experience, etc., required for board members, including knowledge of general business, as well as wide-ranging insight and a high degree of expertise gained through duties experienced inside and outside the Company.

After this, the information necessary for shareholders in their selection is appropriately provided in reference materials for ordinary general meetings of shareholders in accordance with laws and regulations.

Accordingly, the Board of Directors is of the opinion that it is unnecessary to add the proposed provision to the Articles of Incorporation.”

Mizuho was basically saying: “just trust us, we select good guys…no special training about governance and the law is needed…and despite what you may think, whatever information we give you (or do not give you) about them is sufficient”.

But the reality is that Mizuho Financial Group’s board is composed of 12 persons, nine of whom have worked at Mizuho for their entire careers. Most of them do not have any experience serving as impartial directors of outside companies, let alone publicly listed ones – but precisely because they have been internally promoted, it would be easy for Mizuho Financial to give them standardized training and update their knowledge before nominating them as director candidates. Moreover, outside perspectives they might gain from third-party training could offset the inevitable insularity that arises from their single-company career paths. As recent events during the financial crisis and at banks as venerated at Barclays and JP Morgan show, in today’s world the banking business is an increasingly risky one fraught with complex compliance, governance, and regulatory issues. Boards need all the fresh insights they can get.

Under these circumstances, one can hardly blame shareholders for wanting to confirm the preparedness, dedication and corporate governance knowledge base of the director candidates they are being asked to vote for.

In conclusion, Japan’s capital markets seem to be entering a new phase, one that will be characterized by improvement of corporate governance practices and more company-shareholder engagement. These changes will be driven by: (a) corporate concerns about low voting approval for certain director appointments and other company proposals, and (b) a growing number of “reasonable” shareholder proposals that gain significant support (even if there are also more odd ones that get little support). The full impact of these changes will take time to occur at the majority of firms, but many Japanese managers are aware that they now inevitable.

"by Nicholas Benes Representative Director of The Board Director Training Institute of Japan"